January 2024 Commentary

December 2023 and Full-Year 2023 Market Performance

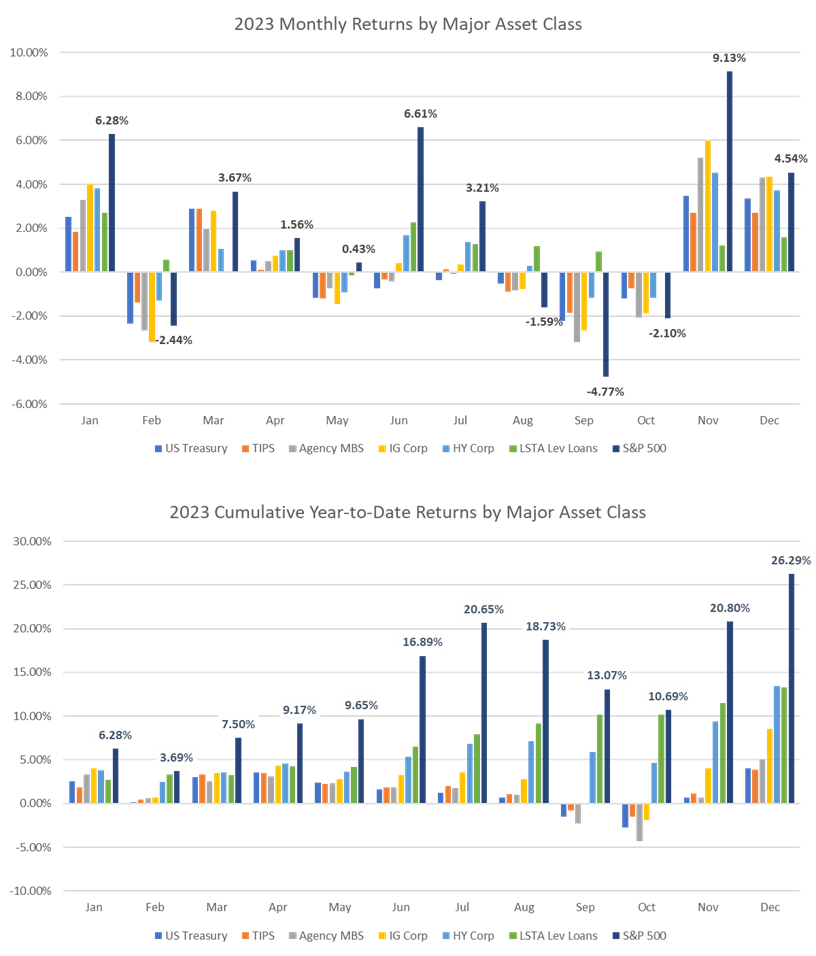

Fourth-quarter returns were largely positive, driven by a belief that the Fed would have to begin cutting rates as early as March 2024. The 10-year UST yield rallied by about 70 bps over the quarter (almost entirely reversing the opposite move in Q3), while the S&P 500 gained 11.7%.

For the full year, all major financial asset classes were positive, with higher-risk assets generating disproportionately higher returns.

Geopolitical volatility has remained notably absent despite the war in the Middle East.

That could easily change if the war expands into a regional conflict.

Exhibit 1. 2023 Monthly and Year-to-Date Returns

Source: Bloomberg, AAFMAA Wealth Management & Trust

Economic and Market Commentary

For several years, AAFMAA Wealth Management & Trust LLC (AWM&T) has offered our clients the option to allocate their exposure to equities through portfolios that invest in primarily dividend-focused stocks or portfolios that focus on expected returns agnostic of dividends. The underlying question behind any such preference — essentially what’s more important, income or return — has captivated investors for decades. In 1961, for example, Merton Miller and Franco Modigliani published a seminal paper that showed that a company’s short-term dividend policy was irrelevant to its valuation.[i] While that result would suggest that portfolio managers largely take other economic and fundamental factors into consideration, there nevertheless, have been legitimate reasons why investors might have preferred at least some exposure to dividend-paying stocks.

We’ve taken an updated look at the historical performance of dividend-focused and dividend-agnostic equity strategies and have concluded that, in isolation, dividend-focused portfolios may not currently offer the advantages they once did. We are confident that now is the time to combine strategies to achieve the best results for our clients and are in the process of beginning that evolution.

In this commentary, we explain more fully why.

The discussion is organized by the top three reasons we believe that investors have been interested in dividend-focused strategies in the past and explanations of why those reasons either no longer apply or may never have been entirely correct. We repeat the following at the conclusion of the commentary, but would like to emphasize it here:

We already have exposure to dividend-paying companies in both the Equity and Equity with Dividend Focus models. Our intention is to blend the Equity- and Dividend-Focused strategies to incorporate the best of “growth at a reasonable price,” value, and dividends in one comprehensive set of strategies. We believe that over the long-term, this approach should provide the most efficient portfolios for our clients.

Here are the most common investor concerns that we’ve heard, and our thoughts based on our updated analysis:

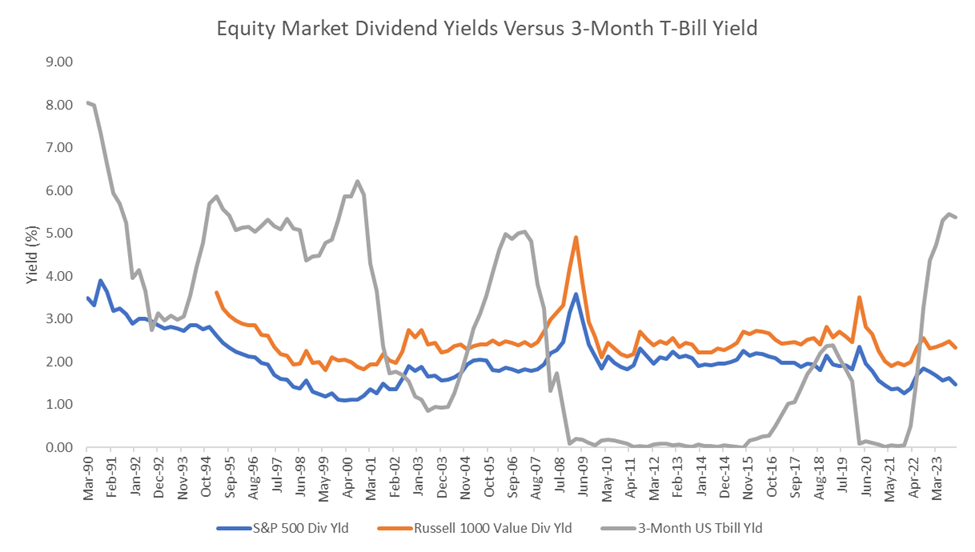

- “I would like current income, but there’s no yield in the bond market. Dividends can substitute for that.” Exhibit 2 compares the historical 3-month US T-Bill yield since 1990 with the dividend yields of the S&P 500 Index and the Russell 1000 Value Index, which is the benchmark for AWM&T’s dividend-focused equity models. As you can see, the Russell 1000 Value Index has consistently paid a higher dividend yield than the S&P 500 — thus its selection as our dividend-focused benchmark. In the post-Great Financial Crisis era (2008 through 2018), equity dividend yields were indeed higher than cash yields. Prior to that, though, dividend yields weren’t higher than cash yields, and they aren’t today either. Investors looking for current income can find it in the cash and fixed income markets. Just as importantly, if the dividends that investors receive are reinvested and not typically distributed in the form of cash, the dividends are not actually providing tangible current income.

Exhibit 2. Equity Dividends Versus Short-Term Interest Rates, 1990 - 2023

Source: Bloomberg, AAFMAA Wealth Management & Trust

Source: Bloomberg, AAFMAA Wealth Management & Trust

- “Dividend-paying stocks are safe because I know that I’m receiving some return in the form of cash. Non-dividend paying stocks are riskier.” While the intuition behind this sounds like it makes sense, there’s no actual evidence that it’s true. In fact, the historical data suggest that there is no relationship between the dividend a company pays and its return (which is consistent with Miller and Modigliani’s findings). To be more precise, (a) the size of a company’s dividend yield has historically been uncorrelated with its current-period return; and (b) there is no relationship between the difference in the size of two companies’ dividend yields and the size of their current-period returns — in other words, companies that pay higher dividends may or may not have higher returns.

Exhibit 3 demonstrates point (a). There has been no discernible pattern between the size of the dividend yield in any quarter and the return over that quarter for the Russell 1000 Value Index. The same is true for the S&P 500.

Exhibit 3. Relationship Between Quarterly Dividend Yield and Stock Return

Source: Bloomberg, AAFMAA Wealth Management & Trust

Exhibit 4 demonstrates point (b). There is no correlation between the difference in two companies’ dividend yields and the difference in their quarterly returns. The chart shows the difference between the Russell 1000 Value Index dividend yield and that of the S&P 500 in each quarter from March 1995 through September 2023 compared with the differences in their quarterly returns.

Exhibit 4. Relationship Between Differences in Quarterly Dividend Yield and Differences in Quarterly Stock Return

Source: Bloomberg, AAFMAA Wealth Management & Trust

- “Companies that have consistently increased their dividend over long periods of time have higher risk-adjusted returns.” This argument is more nuanced. There have actually been periods when this statement has been true, and it’s been the most compelling of the arguments for pursuing a dividend-focused strategy. Over the past 15 years, however, the stocks of companies that consistently grow their dividends haven’t experienced higher risk-adjusted returns. To clarify, “risk-adjusted return” means the ratio of the expected excess annual return of a stock or fund over the risk-free rate to its annualized volatility. We can think of this as a measure of how much return we can expect per unit of risk that we take when we invest in a stock or fund. This measure is called the Sharpe Ratio. The top chart below shows average annual return for the last three-, four-, five-, 10-, 15-, 20-, and 30-year periods for the S&P 500 Index, the S&P 500 Dividend Aristocrats Index, and the Russell 1000 Value Index.

The S&P 500 Dividend Aristocrats Index is an index designed specifically “to measure the performance of S&P 500 index constituents that have followed a policy of consistently increasing dividends every year for at least 25 consecutive years.” That makes it highly representative of the dividend-focused universe of companies. As the chart demonstrates, the S&P 500 has enjoyed higher average annual returns than either the Dividend Aristocrats or the Russell 1000 value indexes for the past three-, four-, five-, 10-, and 15-year periods. Over longer periods, the dividend-focused strategy had higher annual returns.

Exhibit 5 shows the Sharpe Ratios for the same indexes over the same periods. For the past three, four, five, 10, and 15-year periods, the S&P 500 has had risk-adjusted returns that were higher than or equivalent to that of the Dividend Aristocrats. Beyond that, the Dividend Aristocrats did have higher risk-adjusted returns.

Exhibit 5. Return and Risk-Adjusted Returns of Large-Cap and Dividend-Focused Equity Benchmarks

Source: Bloomberg, AAFMAA Wealth Management & Trust

During all the periods in the charts, the S&P 500 had both higher returns and higher risk-adjusted returns than the Russell 1000 Value Index.

We therefore believe that equity strategies that take dividends into account but focus on risk-adjusted returns will have long-term benefits over purely dividend-focused strategies.

As we commented above, we already have exposure to dividend-paying companies in both the Equity and Equity with Dividend Focus models. Our intention is to blend the Equity and Dividend-Focused strategies to incorporate the best of “growth at a reasonable price,” value, and dividends in one comprehensive set of strategies. We believe that over the long term, this approach should provide the most efficient portfolios for our clients.

Yours In Trust,

Paul

[i] Miller, Merton H., and Franco Modigliani. “Dividend Policy, Growth, and the Valuation of Shares.” The Journal of Business, vol. 34, no. 4, 1961, pp. 411–33. JSTOR, http://www.jstor.org/stable/2351143. Accessed 16 Jan. 2024.

Advance Your Finances with AWM&T

You deserve guidance from military financial professionals who demonstrate extensive knowledge, ethical standards, and a commitment to your best interests. Financial planning is more than just numbers — it’s about securing your future and ensuring peace of mind. Speak with one of our credentialed professionals today to get personalized guidance tailored to your unique situation. Visit aafmaatrust.com or call 1-910-307-3500 to learn more.

About Us

Founded in 2012, AAFMAA Wealth Management & Trust LLC (AWM&T) was created to meet the distinct financial needs of military families. We proudly deliver experienced, trustworthy financial planning, investment management, and trust administration services – all designed to promote lasting security and independence.

We are proud to share the mission, vision, and values of Armed Forces Mutual, our parent company. We consistently build on the Association’s rich history and tradition to provide our Members with a source of compassion, trust, and protection. At AWM&T, we are committed to serving as your trusted fiduciary, always putting your best interests first. Through Armed Forces Mutual's legacy and our financial guidance, we provide personalized wealth management solutions to military families across generations.

© 2024 AAFMAA Wealth Management & Trust LLC. Information provided by AAFMAA Wealth Management & Trust LLC is not intended to be tax or legal advice. Nothing contained in this communication should be interpreted as such. We encourage you to seek guidance from your tax or legal advisor. Past performance does not guarantee future results. Investments are not FDIC or SIPC insured, are not deposits, nor are they insured by, issued by, or guaranteed by obligations of any government agency or any bank, and they involve risk including possible loss of principal. No information provided herein is intended as personal investment advice or financial recommendation and should not be interpreted as such. The information provided reflects the general views of AAFMAA Wealth Management and Trust LLC but may not reflect client recommendations, investment strategies, or performance. Current and future financial environments may not reflect those illustrated here. Views of AAFMAA Wealth Management & Trust LLC may change based on new information or considerations.

Get In Touch!

Schedule a consultation with one of our expert financial planners today, and let's hit the fast-track to success!

Schedule A ConsultationRelated posts

May 2024 Market Commentary

Read more

February 2024 Market Commentary

Read more