When my children were young, they had picture books that also had small electronics built into the cardboard pages. Press a certain part of the book, and a small sound file would play. One of our favorites was the Star Wars book with the sounds of lightsabers, X-wing fighters, wookies growling, and the heavy breathing of Darth Vader. The boys’ favorite sound, though, was attributed to Han Solo. As Luke scored his first hit on an enemy-attacking star fighter in the Millennium Falcon, Han cautioned, “Don’t get cocky!” I’m reminded of Harrison Ford’s admonition to stay humble every day as an investor.

Since the June 16, 2022 lows, the S&P 500 rose 12.7%. Our internal asset allocation models noted some relative value for equities versus bonds in June. I noted to colleagues and on social media that if the market had closed on June 16, June would have been the fifth worst monthly showing in 35 years – counting October 1987, August 1998, October 2008, and March 2020 as its downside competitors. But June did not end that day. The rally that began the next day continued throughout the month of July. As markets have recovered some of their losses from earlier in the year, I am reminded again of Harrison Ford’s rebuke: “Don’t get cocky.”

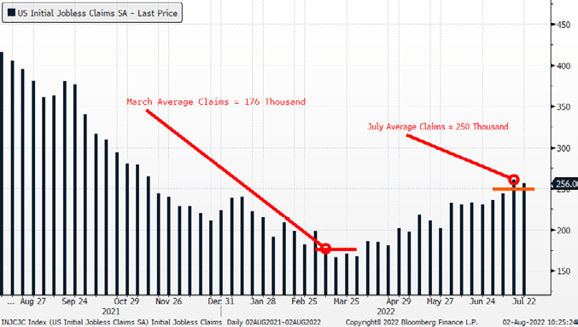

In July, data points began emerging that indicated early evidence that the Federal Reserve’s taps on the economic brake pedals were starting to have their intended effects. Initial jobless claims rose to average 250 thousand per week in July, from their recent low of 176 thousand in March. Continuing unemployment claims continued to rise as well, albeit slowly. While government data has not shown widespread layoffs as of yet, tech companies have started announcing hiring freezes. Anecdotal evidence of hiring freezes stands in stark contrast to a recent hiring survey from Robert Half. Hiring managers reported that 92% of the 1,500 respondents expected to fill either existing vacancies or new positions this year. Only 8% expected to need to lay off employees. The labor market is still very strong.

Inflation continued to accelerate as of the June report received in July. Inflation in the United States grew to 9.1% and inflation in Europe grew to an 8.6% annual pace. With inflation accelerating and few signs of slack in the labor force, the Federal Reserve has a long runway to raise interest rates to achieve its stated policy objective of returning inflation to the range of 2% to 2.5%. Accordingly, the Federal Reserve raised interest rates 0.75% to a range of 2.25% to 2.5%.

Astonishingly, the July narrative expressed by market participants posits that the Federal Reserve will be successful sooner than originally expected in engineering a slowdown in the pace of inflation. As such, the Federal Reserve can begin to slow the pace of rate increases. Moreover, the market-based measures of future rates and inflation expectations have moved so substantially in recent weeks that instead of expecting an aggressive monetary policy for longer, the futures markets now price in the probability of a Federal Reserve that will “pivot” to lowering rates as early as next year!

Inflation is a lagging indicator. The effects of monetary and fiscal policy do not show up immediately in the level of prices in the economy. While I agree generally that quantitative tightening and raising interest rates will ultimately be successful, the recent moves in stock and bond markets seem unrealistically euphoric to me in the short-run.

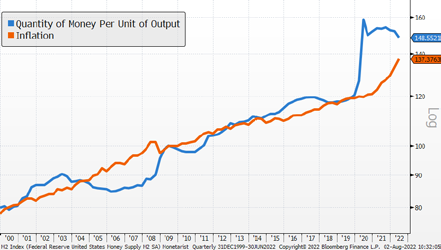

The “Monetarist” chart that I included in my Mid-Year Webinar is updated and included here. The blue line (money per unit of economic output) is declining as the Federal Reserve is shrinking the money supply faster than the economy contracts. The orange line (inflation) is continuing to accelerate as inflation lags monetary policy. It takes time for inflation to respond to monetary expansions and contractions. We didn’t get 9.1% inflation overnight, and we’re not going to get back to 2% inflation quickly either.

In my July webinar and in previous commentaries, I’ve also spoken and written about two other issues. We continue to focus on the War in Ukraine and China. The War in Ukraine may not feature prominently on the front page due to domestic politics coming into the November mid-terms and a recent drop in the price of oil and domestic natural gas. However, the drawdown of the Strategic Petroleum Reserve comes to a close this fall. In addition, elections and electricity rationing in Europe will focus on the side effects of the conflict. We anticipate that staying focused on the war and its economic impacts will be important for investors.

The Chinese economy continues to suffer – not just from the “COVID-Zero” policy which has led to yet another quarantining of over one million people in Wuhan – but also from a real estate mortgage crisis we do not yet fully understand. The Chinese government has become more antagonistic of late. A trip planned by Speaker of the House Nancy Pelosi and the passage of the CHIPS Act exhibit intensified competition between Chinese and U.S. interests vis a vis Taiwan. Strained Chinese/U.S. relations do not benefit either country or economy, let alone the globe.

Stepping away from doom and gloom for a moment, there is good news so far in corporate earnings. Companies have not painted the dire picture that we thought might emerge. Managements are talking about the three themes we expected them to talk about: (1) supply chain, (2) cost inflation from shortages, inventories, and labor, and (3) unfavorable exchange rates. While talking about those things, the companies that have reported thus far have generally met or exceeded Wall Street estimates for corporate profits showing the continued resilience and inventiveness of U.S. companies. Only three of twenty-two companies we own in our main client stock strategies that have reported results as of the end of July have disappointed. More to come though – don’t get cocky!

In my Mid-Year webinar, I talked about the three big issues: (1) the Federal Reserve policy mistake, (2) the energy spike, and (3) the geopolitical crisis of an economically faltering, COVID-Zero, sabre rattling China. In May, I wrote that any one of these issues was enough to cause a recession. And here we are. July marked the release of second quarter GDP. Although the National Bureau of Economic Research (NBER) is the ex-post arbiter of beginning and ending dates for recessions, two quarters of negative real growth is a shorthand that should be sufficient.

The U.S. economy is contracting. Inflation is higher than at any time in the past forty years. Earnings are good, but not great. Unemployment has only recently begun to drift higher. Yet stock markets and bond markets are rallying as if the Fed has already achieved its goals. To those partying and getting aggressively bullish here, I repeat my earlier refrain. Don’t get cocky.

Last month, we talked about your investment objectives and planning for the long-run. We remain cautious across investment objectives and are looking for opportunities to reduce risk in client portfolios. July’s euphoric bear market rally may have given us such an opportunity. However, we will not be completely out of the markets. Investors who run for the hills have to make two problematic timing decisions: when to get out and when to get back in. Our approach is to apply relative value concepts to asset allocation around central allocation targets that match the client’s individual long term goals and objectives. Manage your risk appropriately and returns will follow. Don’t get cocky!

Yours in trust,

At AAFMAA Wealth Management & Trust, we are dedicated to making your financial future as secure as possible. We provide all you need to know about post-retirement military wealth management, starting with a free portfolio review. We strive to learn about your goals and your level of risk tolerance and help you chart your course, build your wealth, and plan your legacy. For all you have done for us, it is the least we can do for you. Your selfless service to our nation deserves our unparalleled military financial service. We salute you.

Related posts

Monthly Market Commentary – October 2022

Read more

Monthly Market Commentary – September 2022

Read more